Apollo

Investment Management

The primacy of resilience

Apollo Asia Fund: the manager's report for 4Q2011

The Apollo Asia Fund's NAV rose 3.1% in the fourth quarter, to US$1,277.06: over

the last twelve months it was up only 0.5%. Portfolio turnover in 2011 was 18%.

At the end of December, our portfolio was on an estimated current-year PE of 13.2,

compared to 11.8 three months earlier. Estimated current portfolio EPS fell almost 8%

during the quarter,

due mainly to the Thai floods, and to one of our holdings which stepped on a small

landmine and will have to write off an investment which it made only a few months ago.

This illustrates one of our fears: the future will be much more

accident-prone than the past. The luck which in the past gave us major winners

will need to hold in future, just to pick our way unscathed through the minefield.

Geographical

breakdown

by listing; 30 Dec 11 |

% of

assets |

| Hong Kong |

12 |

| Japan |

12 |

| Malaysia |

16 |

| Singapore |

29 |

| Thailand |

15 |

| Net cash

& receivables |

16 |

| |

100 |

Weather-related catastrophes in Asia more than tripled over the 30 years to 2010,

and in China more than quadrupled, according

to MunichRe, with a striking chart on page 3 of this pdf file. The company previously

noted that the number of flood disasters globally more than tripled over the

same three decades, and windstorm disasters more than doubled. While noting that

the associated losses were exacerbated by rising population, more people moving

into exposed areas, and higher property values, the company considers that the

rising number of incidents is clearly due to climate change.¹

Quite apart from global warming, we in South-East Asia have seen remarkable changes

in rainfall patterns in recent decades, due to over-development (too much concrete,

too few remaining trees). The fallout is exacerbated by a lack of environmental

understanding (of slope stability, erosion, natural drainage systems and buffers).

At the same time, pollution effects are mounting (eg constant haze, and frequent

smogs²).

The direct economic costs of environmental negligence appear to be rising fast.

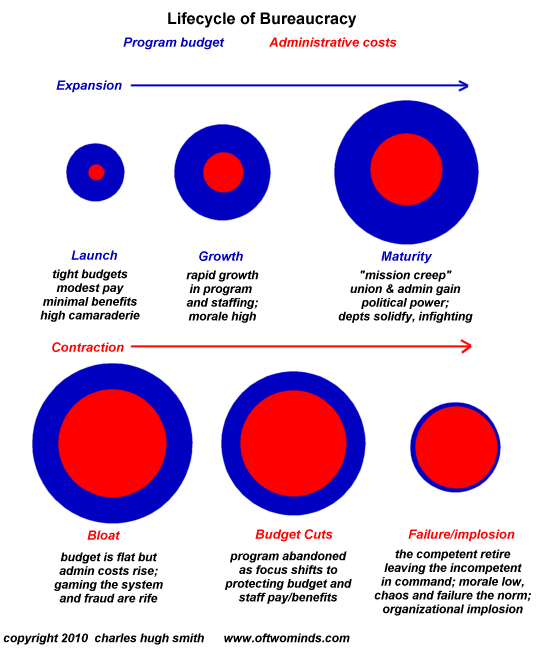

Readers may remember the

graphic

illustrating how the bureaucratic burden frequently expands

to take so much of the economic pie that, even when GDP is still growing, real value

added or the quality of life may be shrinking. Similar arithmetic models may be applied

to falling resource yields (more and more energy and resources go into the process of

extraction, leaving a shrinking net surplus); to the pollution and blowback costs of

eco-contempt; and to the maintenance costs of over-complex systems. Examples are

more and more frequently in evidence.

It seems increasingly desirable to abandon the goal of 'growth' and focus on 'development',

even in those societies where growth is still possible. In practice, it also seems very

difficult to form any new consensus. The likelihood is that policies and goals will become

steadily less coherent, the absurdities and contradictions increasingly evident, and that

we will all have to muddle through as best we can. As investors, our task will be to find

companies and managers with the resilience to survive, and ideally prosper, in increasingly

chaotic conditions.

Masters of strategic adaptability include Asia's

mimic octopus

and jawfish. See them while you can.

Claire Barnes, 8 January 2012

- A recent Chatham House report,

'Preparing

for high-impact, low-probability events', argues that the increasing frequency

of such events (Katrina, Macondo, Eyjafjallajkull, Tohoku) 'signals the emergence

of a new "normal" - the beginning of a crisis trend'; that governments are

woefully unprepared, and that too little attention has been paid to resilience.

- As

in South Asia...

and in

North Asia...

Previous reports:

- 16 Oct 11 Not a normal cycle:

3Q11 report for Apollo Asia Fund

- 26 Jul 11 Open letter

to Securities Commission Malaysia: feedback on Corporate Governance Blueprint

2011

- 22 Jul 11 Bureaucracy and

overcomplexity: 2Q11 report for Apollo Asia Fund

- 8 Apr 11 World in

upheaval: 1Q11 report for Apollo Asia Fund

- 8 Jan 11 Unsustainable

growth: 4Q10 report for Apollo Asia Fund

- 8 Oct 10 More bull:

3Q10 report for Apollo Asia Fund

- 4 Jul 10 Real-world

turbulence, market lull: 2Q10 report for Apollo Asia Fund

- 5 Apr 10 Limits to

growth: 1Q10 report for Apollo Asia Fund

- 23 Mar 10 Energy for Asia:

an overview

- 11 Jan 10 Dangerous times:

4Q09 report for Apollo Asia Fund

- 5 Oct 09 Vertigo again:

3Q09 report for Apollo Asia Fund

- 6 Jul 09 A major bounce:

2Q09 report for Apollo Asia Fund

- 7 Apr 09 Falling prices,

long-term value: 1Q09 report for Apollo Asia Fund

- 6 Jan 09 Tortoise

still crawling: 4Q08 report for Apollo Asia Fund

- 6 Oct 08 Crisis and

opportunity: 3Q08 report for Apollo Asia Fund

- 7 Aug 08 Thai

dividend taxation and NVDRs

- 13 Jul 08 Tectonic shifts:

2Q08 report for Apollo Asia Fund

- 10 Apr 08 The turn of the

stockpicker: 1Q08 report for Apollo Asia Fund

- 11 Jan 08 More interesting

times: 4Q07 report for Apollo Asia Fund

- 8 Oct 07 Complacency

and euphoria: 3Q07 report for Apollo Asia Fund

- 6 Jul 07 The

fully-invested bear: 2Q07 report for Apollo Asia Fund

- 13 Apr 07 The case for

long holidays: 1Q07 report for Apollo Asia Fund

- 6 Jan 07 Thai-phoon

battered: 4Q06 report for Apollo Asia Fund

- 6 Oct 06 Snakes and

ladders: 3Q06 report for Apollo Asia Fund

- 5 Jul 06 To the top

and down: 2Q06 report for Apollo Asia Fund

- 7 Apr 06 Climbing a wall

of irritations: 1Q06 report for Apollo Asia Fund

- 7 Jan 06 Slower growth,

relative value: 4Q05 report for Apollo Asia Fund

- 4 Oct 05 Liquidity

and haze: 3Q05 report for Apollo Asia Fund

- 5 Jul 05 Calm before

the storm?: 2Q05 report for Apollo Asia Fund

- 4 Apr 05 Limitations

in a growing investible universe: 1Q05 report for Apollo Asia Fund

- 7 Jan 05 A time to

recognise good fortune: 4Q04 report for Apollo Asia Fund

- 10 Oct 04 North-east

monsoon approaching: 3Q04 report for Apollo Asia Fund

- 9 Oct 04 Accounting

& disclosure issues in Asia

- 6 Jul 04 Relative

calm: 2Q04 report for Apollo Asia Fund

- 4 Apr 04 Risk

warnings still in force: 1Q04 report for Apollo Asia Fund

- 7 Jan 04 Fun

while it lasts: 4Q03 report for Apollo Asia Fund

- 4 Oct 03 Rise

extended: 3Q03 report for Apollo Asia Fund

- 4 Jul 03 Apollo

in wonderland: 2Q03 report for Apollo Asia Fund

- 6 Apr 03 Turbulent

times, but underlying growth continued: 1Q03 report for Apollo Asia Fund

- 10 Mar 03 Pirates attempt

to seize whole Armada: pitfalls of investing in Malaysia

- 3 Jan 03 A new

high & cautious optimism: 4Q02 report for Apollo Asia Fund

- 17 Oct 02 Relative

resilience: 3Q02 report for Apollo Asia Fund

- 8 Jul 02 A good

harbour: 2Q02 report for Apollo Asia Fund

- 4 Apr 02 Awash

with liquidity: 1Q02 report for Apollo Asia Fund

- 4 Jan 02 Steady

as she goes: 4Q01 report for Apollo Asia Fund

- 10 Oct 01 Resilience

in adversity: 3Q01 report for Apollo Asia Fund

- 5 Jul 01 Prices

more volatile, value still compelling: 2Q01 report for Apollo Asia Fund

- 3 May 01 Opportunities

for selective investors in Asia: article for the Gloom, Boom & Doom

Report

- 13 Apr 01 Earnings

yield 19%; some risk discounted: 1Q01 report for Apollo Asia Fund

- 5 Jan 01 High

seas now evident - how we navigate: 4Q00 report for Apollo Asia Fund

- 10 Oct 00 Tidal waves

forecast, two stocks revisited: 3Q00 report for Apollo Asia Fund

- 6 Jul 00 Price

stagnation, sensational valuation: 2Q00 report for Apollo Asia Fund

- 9 Apr 00 A Pacific

Century - if not for Cyberworks: 1Q00 report for Apollo Asia Fund

- 9 Jan 00 Excellent

values for interesting times: 4Q99 report for Apollo Asia Fund

- 11 Dec 99 Angel of

mercy, or falling angel? Strange happenings at Quality HealthCare

- 14 Nov 99 Apollo Asia

Fund: key terms & summary of features (updated 21 Oct 02)

- 18 Oct 99 Interesting

times ahead! & hence, opportunity: 3Q99 report for the Apollo 001

Fund

- 16 Sep 99 Opacity,

the Asian way? Stock exchange responsibilities on disclosure

- 6 Sep 99 The

all-way case for Asian investment

- 5 Sep 99 Our

type of company - and our type of valuation. A two-stock comparison

- 5 Sep 99 UAF

& Euroclear: lessons and issues

- 4 Sep 99 More

on dollar cost averaging

- 27 Jul 99 After gains,

value persists: 2Q99 report for the Apollo 001 Fund

- 6 May 99 Portfolio

value: an update

- 30 Apr 99 Investment

grade markets, and the imperatives of the herd

- 18 Apr 99 Value, not

momentum: extracts of 1Q99 report for the Apollo 001 Fund

- 3 Mar 99 Perfidious

Thais

- 16 Jan 99 The benefits

of dollar cost averaging

- 16 Jan 99 How good

is the investment case for Asia now?

- 31 Dec 98 Extracts

of manager's 4Q98 report for the Apollo 001 Fund

- 27 Dec 98 Nuggets on

rereading my book, Asia's Investment Prophets

{kind=link}