Apollo Asia Fund's NAV fell 3.5% in the third quarter, to US$2,052.30. It was up 2.3% year-to-date, and has been hopping on the spot since a tumble last October (2018). It may seem surprising that the decline has not been more dramatic, given the magnitude of political shocks on multiple fronts, and new questions over the social stability and public order which investors often take for granted.

Our shares in Hong Kong, India, Indonesia and Thailand all fell. These declines were partially offset by gains in Vietnam, deemed to be a short-term beneficiary of a trade war from which there may be few long-term winners. Many of our holdings, and other prospective investments, in the less fashionable and poorer-performing markets now look cheap by historical standards, if one could assume profitability rebounding to normal historical levels after a bad year or cycle. The uncertainties on many fronts now make it unlikely that the New Normal will look exactly like the Old Normal. Past crises which were predominantly financial now seem simple by comparison. However, we have for some time been prizing resilience, and seeking management teams with the flexibility to build and strengthen comparative advantages which may permit their companies to adapt and thrive.

| Geographical

breakdown by listing; 30 Sep 19 |

% of

assets |

| Hong Kong | 18 |

| India | 1 |

| Indonesia | 5 |

| Japan | 9 |

| Malaysia | 7 |

| Singapore | 0 |

| Thailand | 12 |

| Vietnam | 28 |

| Other | 11 |

| Net cash & receivables | 8 |

| Rounding | 1 |

100 |

The scale and duration of the Hong Kong protests surprised us (and, evidently, the HK government). So many people are better placed to comment (although often constrained); I merely observe, with deep concern.¹ One thing not lacking has been media coverage.

India's militarised constitutional coup in Kashmir, although of little direct relevance to listed companies, may have equally worrying implications and eventual political consequences, but faded rapidly from the headlines, due to travel restrictions and a multi-month clampdown on all communication channels, as well as a much smaller base of international familiarity. The possible return of a Rajapaksa presidency has prompted new fears for Sri Lanka and the implications for India. Pacific islands have been playing China cards against Australia, which has already caused interesting moments for our holding in Oil Search. Japan-Korea tensions are worrying, as is rising nationalism. Against this dramatic backdrop, it is possible that events in the Middle East could prove of greatest historical and global significance: for example the demonstrations of oil infrastructure vulnerability caused by tanker attacks, seizures, and the missile holes in Saudi Arabia's oil processing capacity. The best analysis I read on this important topic has been by Matt Mushalik: see especially 'The Attacks on Abqaiq and Peak oil in Ghawar'; and his most recent article covering amongst other things the strategic vulnerability resulting from Asia's growing dependence on Middle Eastern oil.

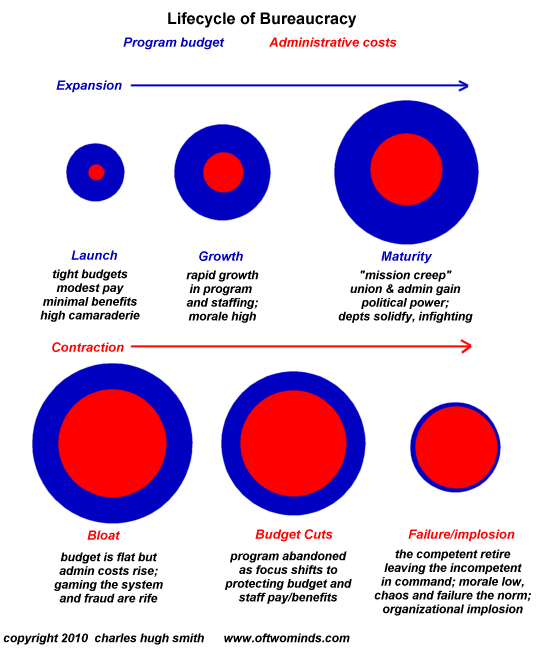

One aspect of corporate resilience is the management capacity to deal with shocks. I noted in my last report the relentless arithmetic of a Hemingway decline: given any finite resource and two competing uses, steady growth in one will eventually lead to accelerating decline in the other. The last report focussed on land use and the crowding out of natural ecosystems; the arithmetic applies equally to time management, and is another way of looking at the burden of bureaucracy, discussed on this site in the past and encapsulated in Charles Hugh Smith's memorable image of the Lifecycle of Bureaucracy. The working day is finite, so if the time taken by unproductive tasks happens to grow steadily, this would lead inexorably to a Hemingway Decline in productive activity.

In recent years our companies have experienced a number of shocks, some very unfortunate but of a familiar type (e.g. the sudden death of a young, healthy and dynamic boss), and some of a type that we had never then anticipated (capricious US actions to lock a company out of its major market on unsupported anonymous allegations, or to seize enormous sums from a company on the other side of the world for doing business in a country that the US dislikes). Extreme environmental shocks and manmade environmental-mismanagement disasters are affecting business continuity planning, as are social unrest and political upheaval. Customer priorities may be changing, and divergent stakeholder responses may affect morale and complicate decisionmaking. Resilience has always seemed important, but we are now paying more attention to management resilience against multiple shocks. Conscientious managers will often rally impressively to fight one threat, but have less energy to deal with the next, and the next - or less capacity to think about issues that may be important but not urgent, and fall behind competitors which are temporarily less beleaguered.

Management depth and succession are always relevant. In a small business, the challenges may (rightly or wrongly) seem relatively straightforward to evaluate. Size may bring depth and momentum, and allow the deployment of additional resources; it can also lead to compartmentalisation and to rigidity. There will be no single recipe for resilience, any more than for initial success; corporate culture remains a mysterious art. Resilience evades quantification, and seems important; it will remain a factor in our stock selection.

As I write, I am cheered by a product of resilience: excellent coffee from Marawi City. Two years after the end of the siege, well over a hundred thousand people remain homeless. Some individuals and small groups are finding new ways to make a living. My coffee is branded Khapeta Marawi, a social enterprise with BMW, the Bangsamoro Movement for Welfare. It proclaims a vision for a better city, and claims impressive health benefits for black coffee, including the reduction of stress and depression. I take this as good authority: they know whereof they speak.

My title proclaims no allegiance: it just seems a helpful image. Heraclitus noted that one never steps in the same river twice. We have imperfect knowledge of the substrate and currents. We need to move forward. It seems sensible to cross the river by feeling the stones.

Claire Barnes, 28 Oct 2019

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |

{kind=link}