NAV of the Apollo Asia Fund fell 5.9% in the third quarter, to US$2,455.97 (Series A). That's down 11.0% year-on-year, but up 20% over three years, and up 53% since March 2020 when markets were beginning to rally after the initial pandemic slump.

Part of the decline came from foreign exchange rates, as the US$ surged against almost all other currencies, including all of the currencies we own. As measured by ADXY, the Bloomberg JPMorgan Asian Dollar Index, Asian currencies fell 5.5%.

|

Share price performance in local-currency terms was mixed, but we saw thumping markdowns in all of our Hong Kong holdings. This was mostly due to general market weakness (the Hang Seng index fell 21%, and our shares overall by slightly less), but there was one special case which may be of interest.

Giordano had risen in June on receiving a takeover approach from the Cheng family. We agreed with David Webb's comment that the offer was far below fair value, and that management should invite competing offers. I have no idea whether they or the independent directors attempted to do so, and no other offer reached the public, but it was reassuring that the key executive directors declared that they would retain their holdings. Independent shareholders took the same view, and the bid was conditional on outright control so it lapsed with no change in the shareholdings. The share price had risen from very depressed to the offer price, and fell back when the offer expired - at which point the company paid its interim dividend, and provided more details of its network expansion in India. This is new, and small in group terms, but the company pointed out that in North India alone it is moving into a market of over 400 million people. We feared that Giordano's far-flung network would be hard to manage in a time of prolonged border closures, but its disciplined risk control and accountant-driven systems appear to have proven a significant competitive advantage. For the last two years all profits have been coming from Southeast Asia and the Middle East - and now it is venturing carefully into Africa and Central Asia. The original businesses in Hong Kong and China have been a drag (loss-making), but clearly retain value. The nominal share price was down 24% over the quarter; adjusting for the usual substantial dividend, the fall was 19%. At the end of September, the multiple of 12-month trailing earnings was 10.8, and the 12-month trailing dividend yield 13.2%.

We think the value here compelling. Consumer demnd for workaday clothing at affordable price-quality points will continue. Supplying it reliably was never easy, and is now tougher than ever, but some management teams in this and in other sectors are rising to the challenges and pulling ahead of competitors. We'll continue to look out for resilient businesses with effective and conscientious leadership, especially when they become available at attractive prices, and welcome suggestions from our readers.

Resilience is key. Protectionism, waning international cooperation, inflation and rising interest rates add to all the previous challenges which include unprecedented debt, ecological crises, and living beyond planetary means. We're in turbulent times.

The quarter ended explosively. The sabotage of the Nordstream 1 and 2 pipelines on 26th September caused huge and deliberate damage to non-combatant European nations. By exacerbating the energy squeeze, it endangers German manufacturing industry, and ensures a very difficult winter for hard-pressed consumers and governments. The political and economic consequences are hard to predict, but modern life depends on pipelines, electrical cables, and telecommunication cables. The world has been living with terrorism by private individuals and groups, but the suspicion that another government planned this cavalier destruction of national infrastructure ratchets risk assessments to a new level. The proportion of global efforts directed to remediation, damage mitigation and security seem likely to increase. Such activities contribute to GDP, but squeeze out spending that would increase prosperity.

| |

|

For international investors, Asia used to be a leveraged play on the world's growth, now uncertain. It used also to be a catch-up play, as one country after another adopted successful practices and moved up the income ladder. Such simple investment cases had become harder to make, with the competitive advantages waning as many countries face ageing populations, resource depletion and other limits to growth. High levels of debt and excessive construction have caused crises in the past, and may do again. However, Asia remains open for business, pragmatic in its energy sourcing, and perhaps still relatively flexible. As investors seek havens, geographical diversification still makes sense, and current US$ strength should increase the attractions of an allocation to Asia.

COVID is a wildcard. Since the economic disruption from both disease and countermeasures has been so great over the last three years, perhaps there is also a case for diversifying into countries with different public health responses? There is concern about the scale of long-term ill health and cognitive impairment resulting from past Covid infections, beyond those who self-report any Long Covid symptoms. This could clearly have implications for workforce productivity and decisionmaking, and may already be a factor in labour shortages in the US and UK. Will Asian countries do better?

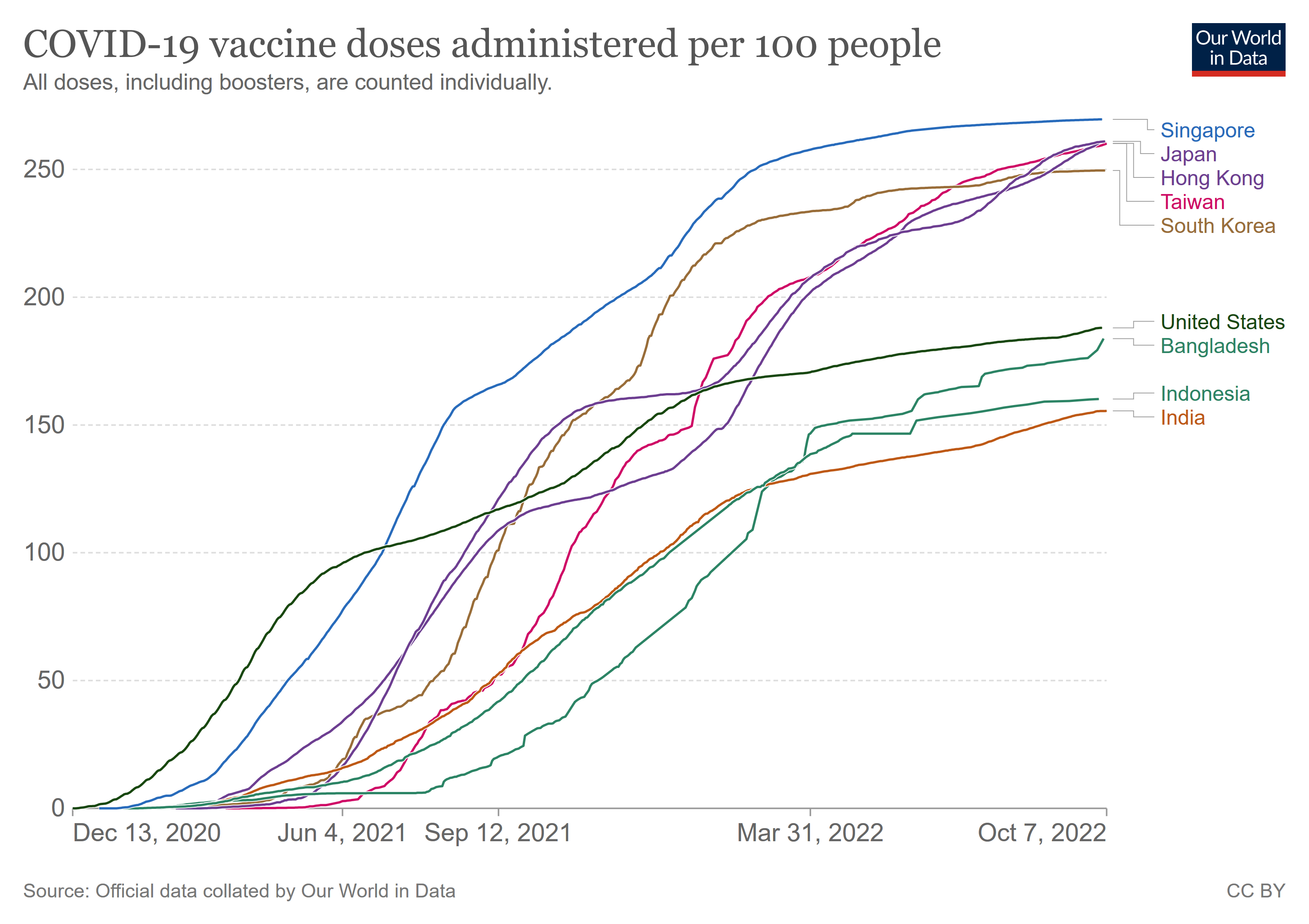

Measured by excess mortality, many have done so to date - and after initial delays in access, many Asian countries now have their populations well vaccinated and boosted. The chart shows Singapore's vaccine alacrity, and the North Asian countries now at high levels after slower initial takeup. It also shows the recent improvement in some very populous countries: Bangladesh, Indonesia and India. (China, Malaysia and Thailand are in between, and omitted for clarity.) Emerging variants may require new vaccines, but it is encouraging that public health systems are now geared up to deliver them at speed and scale.

Production of the patent-free, low-cost, regular-temperature Texas vaccine has been increasing, as Corbevax in India (75 million doses administered, ramping capacity to 1 billion) and as Indovac in Indonesia (20 million produced). It is hoped that this will bring affordable vaccines to the rest of the world: a noble goal. Meanwhile, the geographical spread of contenders in the race for mucosal vaccines is strikingly diverse: Asian companies are also innovating. Asia has 60% of the world's population, and as others stumble, its influence in the world is increasing.

Good health to all our readers.

Claire Barnes, 10 October 2022

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |