Apollo

Investment Management

Overcomplexity to dysfunctionality

Apollo Asia Fund: the manager's report for 3Q2013

The Apollo Asia Fund's NAV fell 0.8% in the third quarter, to US$1,896.80. Over the last twelve

months it was up 9.3%.

Despite a 5% retreat in NAV from the peak in May, the estimated current-year PE of the fund at the

end of September was 15.6, still relatively high by the fund's own historical standards. Moreover, some

of the high-quality, cash-generative consumer stocks which have stood us in good stead in the past

are now priced for ongoing high growth which we doubt they will be able to deliver, and many of

the stocks less highly rated are discounted for good reason. Stock selection currently seems

quite challenging.

Geographical

breakdown

by listing; 30Sep13 |

% of

assets |

| Hong Kong |

18 |

| Japan |

16 |

| Malaysia |

10 |

| Singapore |

19 |

| Thailand |

11 |

| Other |

9 |

| Net cash

& receivables |

17 |

| |

100 |

Moreover, a growing proportion of our attention goes to monitoring (and trimming)

our existing holdings, many of which seem to be finding their own businesses equally

challenging.

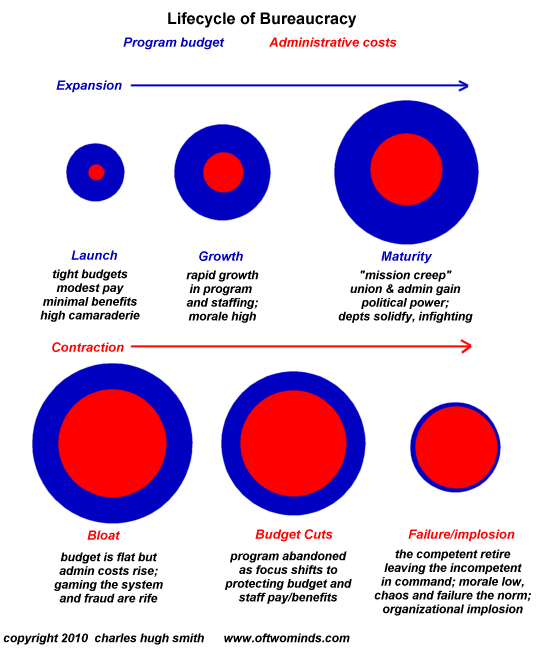

Our report in July 2011 discussed bureaucracy and overcomplexity,

highlighting

this graphic

illustrating an issue which appears more and more relevant.

The complexity of simple tasks and services seems to be growing apace.

More and more detailed regulation is crowding out useful activity.

More and more professional people seem to be swamped - and to have less and less time

remaining to focus on the most important aspects of their jobs.

More and more systems seem to be tipping from overcomplexity to dysfunctionality.

Fascinating examples have arisen in recent weeks.¹ ²

There must be beneficiaries of this somewhere. Individual lawyers, regulators, and

fixers are hard to invest in. Some IT companies, conference organisers, printing

companies and hotels may benefit - but these are not particularly promising sectors for a fund such as ours.

Related issues, which might be addressed in analogous diagrams,

include the rising costs of environmental damage and resource extraction.

These also tend to benefit GDP in the short run, but leave a dwindling percentage of it

representing more useful activity. Similarly, if individuals are becoming wealthier on paper, but

a growing percentage of their income is consumed by food, housing, transport and debt service,

they may find their real disposable incomes dropping. Companies providing the essentials may

prove to be attractive investment propositions, but it seems increasingly important to recognise

that a continuous rise in living standards is not to be taken for granted. The Asian countries

in which we invest have had an extraordinary few decades; straight-line extrapolation remains

common, but we try to avoid it. Encouragingly, there seems to be a slight increase in discussion

about the difference between growth and development, about resource constraints of various types,

and about more appropriate goals for society. It will probably take a long time for these debates to translate into

action. If the pie is no longer growing rapidly then distribution will become more complex; meanwhile,

political tensions may continue to rise.

In the last quarter we have been trimming and exiting a number of long-held

positions, for various reasons:

- A & B. High valuation; lack of ideas or opportunities to generate as much growth as the market expects.

- C. High valuation; sector growth ultimately unsustainable, although consensus does not see any problem.

- D. Temporary slow growth generating board/management fissures, and an unnecessary panic to achieve the impossible. Individuals acting in good faith take bad decisions leading to downward spiral of lower valuation and further bad decisions. Leadership adequate for previous growth phase but not up to the current challenges - which makes it difficult to strengthen the team appropriately. Deep value remains in an extraordinarily profitable

cash-generating business, but current decision-making seems likely to dilute the characteristics that originally attracted us.

- E&F. Loss of confidence that controlling shareholder will look after interest of minority investors. In the first case, this is an individual, an entrepreneur. In the second, the controlling shareholder is another listed company, ultimately government controlled, and should be setting a better example.

In this second and more interesting case, poor executive and board appointments

have led to a sharp deterioration in decision-making ability. The new managing director may be a loyal servant of the parent, but is oblivious to the many growth opportunities in the region. Disclosures have been progressively slashed. In a meeting arranged with great difficulty, it was explained that this was in case regulators / competitors / customers start to resent the company's profitability - it is apparently assumed that they will be more relaxed about the profitability of a black box. The new culture of secrecy and obfuscation does not appear helpful to internal clarity on the issues that matter, or to constructive engagement with the outside world where new opportunities might arise; the corporate culture is regressing into ineffective bureaucracy.

In the former cases, where the concern is valuation, but the underlying businesses

are still of high quality, we have been gradually selling down but (as yet) not out. The cases

where the business is deteriorating are of greater concern, and command greater attention.

When we lose confidence in integrity or governance, we try to exit as soon as possible, so

the two latter holdings have gone.

The companies we like are those which have continued ability to grow

and a clear plan of action which we believe they will be able to implement steadily,

adjusting to inevitable gusts, but able to maintain a steady course even in changing

circumstances. Any well-run company of this type

is one that we would like to have on the radar screen, as analysis often takes us

months; we can then be in a position to buy when valuations are fair or better.

We have a number of these, and have added one new one recently. We have many more

candidates on the watchlist or yet to research, but are always happy to hear of more.

Claire Barnes, 3 Oct 2013

- A leading bank directs card applications to be made online.

Almost all such applications fail.

When a human can be found, after the usual half hour navigating a robotic call centre,

it transpires that the bank knows this, and recommends calling an individual on a

mobile phone. Does this individual actually work for the bank? Who knows?

The systems are so complicated that they have to be bypassed.

Meanwhile, the marketing department, or the computers, continue to send out instructions

that are known to fail; and the customers continue to spend weeks in pointless activity.

Expensive advertising campaigns seek to build an impression of brand quality.

Officials marketing the bank's corporate services now have a new marketing

proposition: to sort out the personal banking woes of individuals who can take decisions

on corporate accounts. The officials may not be able to navigate their internal systems

either, but the worse the personal banking services, the more attractive the offer.

And it is easier than arguing the

merits of the corporate banking services, or sorting out the deficiencies there...

- Visas. Becoming more time consuming for many countries, and I doubt

that the increased complexity helps national security. My last visa for India took more

of my time to procure than I spent in the country (attention time, not processing time).

Getting the latest one was much, much more complicated.

I will try to use it to the full, and to avoid for as long

as possible the need to apply for another. This country wishes to encourage foreign

investment, and has expensive marketing campaigns to encourage tourism?

Previous reports:

- 7 Jul 13 Ominous tremours:

2Q13 report for Apollo Asia Fund

- 6 Apr 13 Good governance

is vital: 1Q13 report for Apollo Asia Fund

- 22 Jan 13 Gaps in the

canopy: suggestions for HSBC's forest policy

- 16 Jan 13 Markets

expensive, complacency dangerous: 4Q12 report for Apollo Asia Fund

- 12 Oct 12 Cognitive

dissonance: 3Q12 report for Apollo Asia Fund

- 16 Jul 12 The imprecision

of vital statistics: 2Q12 report for Apollo Asia Fund

- 4 Apr 12 Nifty

valuations: 1Q12 report for Apollo Asia Fund

- 8 Jan 12 The primacy

of resilience: 4Q11 report for Apollo Asia Fund

- 16 Oct 11 Not a normal cycle:

3Q11 report for Apollo Asia Fund

- 26 Jul 11 Open letter

to Securities Commission Malaysia: feedback on Corporate Governance Blueprint

2011

- 22 Jul 11 Bureaucracy and

overcomplexity: 2Q11 report for Apollo Asia Fund

- 8 Apr 11 World in

upheaval: 1Q11 report for Apollo Asia Fund

- 8 Jan 11 Unsustainable

growth: 4Q10 report for Apollo Asia Fund

- 8 Oct 10 More bull:

3Q10 report for Apollo Asia Fund

- 4 Jul 10 Real-world

turbulence, market lull: 2Q10 report for Apollo Asia Fund

- 5 Apr 10 Limits to

growth: 1Q10 report for Apollo Asia Fund

- 23 Mar 10 Energy for Asia:

an overview

- 11 Jan 10 Dangerous times:

4Q09 report for Apollo Asia Fund

- 5 Oct 09 Vertigo again:

3Q09 report for Apollo Asia Fund

- 6 Jul 09 A major bounce:

2Q09 report for Apollo Asia Fund

- 7 Apr 09 Falling prices,

long-term value: 1Q09 report for Apollo Asia Fund

- 6 Jan 09 Tortoise

still crawling: 4Q08 report for Apollo Asia Fund

- 6 Oct 08 Crisis and

opportunity: 3Q08 report for Apollo Asia Fund

- 7 Aug 08 Thai

dividend taxation and NVDRs

- 13 Jul 08 Tectonic shifts:

2Q08 report for Apollo Asia Fund

- 10 Apr 08 The turn of the

stockpicker: 1Q08 report for Apollo Asia Fund

- 11 Jan 08 More interesting

times: 4Q07 report for Apollo Asia Fund

- 8 Oct 07 Complacency

and euphoria: 3Q07 report for Apollo Asia Fund

- 6 Jul 07 The

fully-invested bear: 2Q07 report for Apollo Asia Fund

- 13 Apr 07 The case for

long holidays: 1Q07 report for Apollo Asia Fund

- 6 Jan 07 Thai-phoon

battered: 4Q06 report for Apollo Asia Fund

- 6 Oct 06 Snakes and

ladders: 3Q06 report for Apollo Asia Fund

- 5 Jul 06 To the top

and down: 2Q06 report for Apollo Asia Fund

- 7 Apr 06 Climbing a wall

of irritations: 1Q06 report for Apollo Asia Fund

- 7 Jan 06 Slower growth,

relative value: 4Q05 report for Apollo Asia Fund

- 4 Oct 05 Liquidity

and haze: 3Q05 report for Apollo Asia Fund

- 5 Jul 05 Calm before

the storm?: 2Q05 report for Apollo Asia Fund

- 4 Apr 05 Limitations

in a growing investible universe: 1Q05 report for Apollo Asia Fund

- 7 Jan 05 A time to

recognise good fortune: 4Q04 report for Apollo Asia Fund

- 10 Oct 04 North-east

monsoon approaching: 3Q04 report for Apollo Asia Fund

- 9 Oct 04 Accounting

& disclosure issues in Asia

- 6 Jul 04 Relative

calm: 2Q04 report for Apollo Asia Fund

- 4 Apr 04 Risk

warnings still in force: 1Q04 report for Apollo Asia Fund

- 7 Jan 04 Fun

while it lasts: 4Q03 report for Apollo Asia Fund

- 4 Oct 03 Rise

extended: 3Q03 report for Apollo Asia Fund

- 4 Jul 03 Apollo

in wonderland: 2Q03 report for Apollo Asia Fund

- 6 Apr 03 Turbulent

times, but underlying growth continued: 1Q03 report for Apollo Asia Fund

- 10 Mar 03 Pirates attempt

to seize whole Armada: pitfalls of investing in Malaysia

- 3 Jan 03 A new

high & cautious optimism: 4Q02 report for Apollo Asia Fund

- 17 Oct 02 Relative

resilience: 3Q02 report for Apollo Asia Fund

- 8 Jul 02 A good

harbour: 2Q02 report for Apollo Asia Fund

- 4 Apr 02 Awash

with liquidity: 1Q02 report for Apollo Asia Fund

- 4 Jan 02 Steady

as she goes: 4Q01 report for Apollo Asia Fund

- 10 Oct 01 Resilience

in adversity: 3Q01 report for Apollo Asia Fund

- 5 Jul 01 Prices

more volatile, value still compelling: 2Q01 report for Apollo Asia Fund

- 3 May 01 Opportunities

for selective investors in Asia: article for the Gloom, Boom & Doom

Report

- 13 Apr 01 Earnings

yield 19%; some risk discounted: 1Q01 report for Apollo Asia Fund

- 5 Jan 01 High

seas now evident - how we navigate: 4Q00 report for Apollo Asia Fund

- 10 Oct 00 Tidal waves

forecast, two stocks revisited: 3Q00 report for Apollo Asia Fund

- 6 Jul 00 Price

stagnation, sensational valuation: 2Q00 report for Apollo Asia Fund

- 9 Apr 00 A Pacific

Century - if not for Cyberworks: 1Q00 report for Apollo Asia Fund

- 9 Jan 00 Excellent

values for interesting times: 4Q99 report for Apollo Asia Fund

- 11 Dec 99 Angel of

mercy, or falling angel? Strange happenings at Quality HealthCare

- 14 Nov 99 Apollo Asia

Fund: key terms & summary of features (updated 21 Oct 02)

- 18 Oct 99 Interesting

times ahead! & hence, opportunity: 3Q99 report for the Apollo 001

Fund

- 16 Sep 99 Opacity,

the Asian way? Stock exchange responsibilities on disclosure

- 6 Sep 99 The

all-way case for Asian investment

- 5 Sep 99 Our

type of company - and our type of valuation. A two-stock comparison

- 5 Sep 99 UAF

& Euroclear: lessons and issues

- 4 Sep 99 More

on dollar cost averaging

- 27 Jul 99 After gains,

value persists: 2Q99 report for the Apollo 001 Fund

- 6 May 99 Portfolio

value: an update

- 30 Apr 99 Investment

grade markets, and the imperatives of the herd

- 18 Apr 99 Value, not

momentum: extracts of 1Q99 report for the Apollo 001 Fund

- 3 Mar 99 Perfidious

Thais

- 16 Jan 99 The benefits

of dollar cost averaging

- 16 Jan 99 How good

is the investment case for Asia now?

- 31 Dec 98 Extracts

of manager's 4Q98 report for the Apollo 001 Fund

- 27 Dec 98 Nuggets on

rereading my book, Asia's Investment Prophets

{kind=link}