The Apollo Asia Fund's NAV fell 5.9% in the fourth quarter, to US$1,916.92, 4.3% down for the year, and almost 10% down from the peak achieved in August. Currency weakness caused us further losses: the Singapore dollar fell 4% during the fourth quarter, the Malaysian ringgit was down 6%, and the yen fell by another 9%. Rightly or wrongly, we remain unhedged. (In 2014, clearly wrongly.)

| Geographical

breakdown by listing; 31 Dec 14 |

% of

assets |

| Hong Kong | 23 |

| India | 5 |

| Japan | 19 |

| Malaysia | 9 |

| Singapore | 12 |

| Thailand | 11 |

| Other | 9 |

| Net cash & receivables | 13 |

| Rounding | -1 | 100 |

In the last quarterly we wrote about the change of control at Tomypak Holdings; we expected that the Securities Commission would require a General Offer and hoped that the independent directors would then rise to the occasion and use the opportunity to open up to competitive bidding. Neither of these happened: the SC decided not to act, the independent directors decided to rubberstamp the appointment of directors proposed by the new shareholders despite track records which cause us some concern, and our nomination of directors to protect the interest of minority shareholders was rejected. We put much effort into this situation over the last nine months, and cannot report any return on that effort: the new shareholders are treating minorities with contempt, and the long-serving independent directors are ineffective. The share price remains depressed on low volume, so it was not a significant contributor to the fund's poor 4Q performance (and fortunately it is one of our smallest holdings) - but the flexible packaging industry has great potential, and this used to be a leader in the sector, so the turn of events is decidedly disappointing.

On 1 Nov the fund changed its administrator, to Apex Fund Services. Although we retained HSBC as custodian, they informed us just before the transition that they would close the bank account used for subscriptions, redemptions and fund expenses. This was unhelpful to put it mildly. Our new account has become fully operational this week. HSBC's once formidable franchise is eroding fast, as they alienate long-standing customers in all sectors and in many countries: we would not wish to be shareholders.

The fund is domiciled in the British Virgin Islands, which has signed Intergovernmental Agreements with the US and the UK imposing new information gathering and reporting requirements on funds and their investors, in relation to the US Foreign Tax Compliance Act ("FATCA") and a growing thicket of related legislation and regulation. There are a number of uncertainties. Some aspects may have come into force on 1 Jan, but the BVI's expected Guidance Notes do not yet appear to have been published. The Explanatory Memorandum of the fund has been updated meanwhile, and attempts to cover all eventualities. It imposes obligations on our investors to respond to any future requests from the fund for additional information that may be required by regulators, and provides for compulsory redemption if the information is not promptly forthcoming or to protect the interests of the fund. We regret being forced to act in this peremptory fashion. The administrator has despatched a letter to investors, informing you of the changes; if you are a shareholder and do not eventually receive this, please let us know, and ensure that we have current contact details.

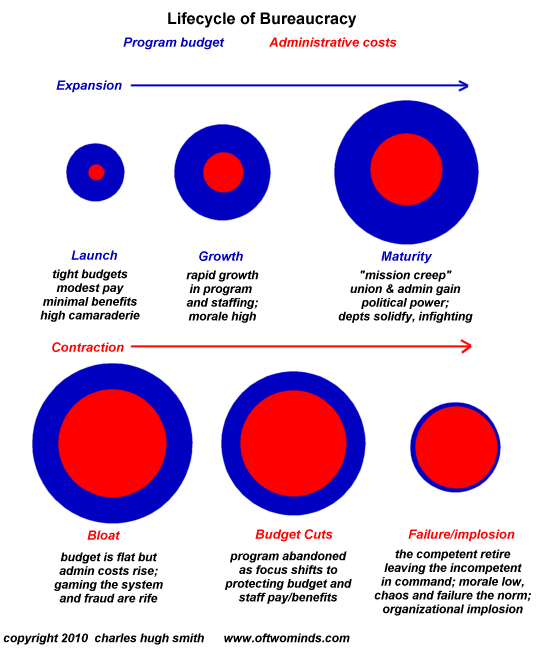

The acronym FATCA is frequently delivered as a swearword because of the extraordinary bureaucratic burden it is imposing on the financial sector around the world, on institutions and individuals who may have nothing to do with the US. The new regulatory environment poses a great many new risks to investors, which I will not attempt to list since I would prefer to be grappling with the even greater number of new challenges in the world outside. One major risk is that the percentage of a fund manager's time spent on bureaucracy and regulation continues to rise until it precludes all useful activity: we refer once again to the graphic on the lifecycle of bureaucracy, now visibly relevant to many businesses and economies.

Amidst all these distractions, I omitted to post a link to GMO's 3Q report, with another compelling exposition from Jeremy Grantham on what I consider the key issue of our time. While acknowledging short term benefits from the fall in the oil price, as income is transferred from producers to consumers with a greater propensity to spend, he explains with great clarity why the current fall in the oil price 'does nothing to offset the squeeze on the total economy from rising costs', and provides some alarming illustrations of the magnitude of that squeeze. We differ on coal: as mentioned here six months ago, the usage of coal in Asia is rising and not falling, as oil and gas production falters. However, Grantham's central message could hardly be clearer - or further from complacent assumptions of business-as-usual. '... other parts of the complex economic system have to be sacrificed to retain the ability to acquire sufficient oil... if oil costs continue to rise the trade-offs become more and more painful. Our complex system has been trained by experience to deal with steady growth. Now it must deal with slowing growth and one day it may face contraction. In this changed world we can only guess how robust the stressed system will be. We may hope it will be tough but quite possibly it will be brittle. At the extreme it might even threaten the viability of our current economic system. It is vital therefore, if we want to reduce these stresses, to emphasize fuel efficiency, reduce wastage of all kinds, and encourage the rapid development of sustainable "alternative" forms of energy... Clearly the writing is on the wall. It is now up to our leadership and to us as individuals to read it and act accordingly.' First read the rest: 'The Beginning of the End of the Fossil Fuel Revolution (from Golden Goose to Cooked Goose)'.

If only we knew how to invest accordingly. Portfolio turnover in 2014 was low, at 12%. With the world in turmoil, we may well need to make more changes in the year ahead. Some of the changes we made earlier have not, as yet, gone to plan. Suggestions, as always, are welcome.

Claire Barnes, 9 Jan 2015

| Home | Investment philosophy | Fund performance | Reports & articles | *What's new?* |

| Why Apollo? | Who's Claire Barnes? | Fund structure | Poetry & doggerel | Contacts |

{kind=link}